Storm chasers are out-of-town roofing contractors who deploy to Cypress after hail and wind events. They’ve become a serious problem for Cypress homeowners because they frequently install cheaper materials than insurance estimates specified, disappear before warranty issues surface, and in some cases leave homeowners with insurance complications that last years. Cypress has become a documented insurance claim hotspot due to repeated hail events in 2024 and 2025, making it a prime target for storm chaser deployment. The most effective protection is choosing a contractor with a permanent Cypress-area presence, a verifiable Texas contractor license, and a physical office address, before you sign anything.

Within 48 hours of the last major Cypress hail event, dozens of out-of-state roofing crews were already working their way through Bridgeland and Towne Lake. Some were legitimate. Many were not. By the time the homeowners figured out the difference, those crews were already in Louisiana chasing the next storm.

This isn’t a hypothetical. On December 24, 2024, a severe hailstorm with stones reaching golf-ball size hit Cypress, damaging over 2,200 homes in a single event. Across Harris County, more than 25,000 homes filed claims within two weeks. [1] Adjuster shortages pushed appointment timelines out by weeks. That window, the gap between the storm and the inspection, is exactly where storm chasers operate.

M&M has been called to Cypress homes as a “second roofer,” brought in after a storm chaser did the initial work, and the roof failed within 6 to 18 months. This article is written from that vantage point. Not to alarm you. To arm you.

Why Cypress Has Become a Storm Chaser Target

Cypress sits in northwest Harris County directly in the path of Gulf-fed supercell storm systems that track northeast through the Houston metro. The area averages more than 50 significant thunderstorm days per year, and the 2024 and 2025 hail seasons were unusually active. Harris County is one of the highest-claim-density counties in Texas for wind and hail damage. [1]

The communities that make up Cypress, Bridgeland, Towne Lake, Fairfield, Coles Crossing, Canyon Lakes West, and Miramesa are relatively new, high-value construction with homeowners who carry comprehensive insurance policies. That combination is exactly what storm chasers are targeting.

Here’s how the storm chaser business model works. These companies aren’t based in Cypress. They’re based in Oklahoma, Tennessee, Louisiana, or wherever their nearest staging area happens to be. When storm radar shows a significant hail event in a high-income suburban market, they dispatch crews within 24 to 48 hours. Those crews work neighborhoods door to door, collecting signed contracts and insurance assignments as fast as possible. Then they follow the next storm wherever it leads.

The economics make sense for them. Whether the work holds up is someone else’s problem. And they won’t be here to deal with it.

The 5 Ways Storm Chasers Actually Burn Cypress Homeowners

These aren’t vague warnings. These are specific mechanisms M&M has documented on Cypress roofs when called in to inspect or repair prior storm chaser work.

1. They Install Cheaper Materials Than Your Insurance Paid For

Your insurance estimate specifies architectural (dimensional) shingles: a thicker, layered product built to last 25 to 30 years. The storm chaser installs 3-tab shingles instead. Thinner, cheaper, with a lifespan of 15 to 20 years under ideal conditions. The homeowner can’t tell the difference from the ground. The storm chaser pockets $800 to $1,500 in the cost difference and leaves.

How to catch it before it happens: ask to see the manufacturer’s packaging before work begins. Your insurance estimate should specify the exact shingle product line, such as GAF Timberline HDZ or Owens Corning Duration. Verify that’s exactly what’s being installed. If the contractor can’t show you the packaging, that’s your answer.

2. They Skip Line Items on the Insurance Estimate

Insurance estimates cover more than shingles. They include flashing replacement, ice and water shield, drip edge, ridge cap, and starter strip. Storm chasers often skip or substitute these items: reusing old flashing, omitting ice and water shield on low-slope transitions, and skipping the drip edge entirely. The homeowner never knows because they don’t know what the estimate includes.

The consequence shows up two to three years later when sections without proper underlayment or drip edge show water intrusion. Before signing any contract, ask the contractor to walk you through every line item on your insurance estimate and confirm in writing that each is included in their scope of work.

3. They Use the Assignment of Benefits to Cut You Out of the Process

An Assignment of Benefits (AOB) transfers your right to insurance proceeds from you to the contractor. Once you sign it, the contractor negotiates directly with your insurer. You have no oversight over what gets claimed, what gets built, or what disputes arise. Storm chasers push AOB agreements aggressively because they can then file supplemental claims without the homeowner’s knowledge. Texas has seen TDI enforcement actions against contractors for AOB abuse. [2]

The rule: never sign an AOB before you have a complete, written scope of work specifying exact materials and costs. Legitimate local contractors do not require AOB agreements to perform standard roof work.

4. They’re Unreachable When Something Goes Wrong

Storm chasers operate nomadically. They don’t have a local Cypress office. Their phone numbers often route to a scheduling center in another state. When a shingle blows off eight months later, or a flashing leak develops the following spring, you call the number on the contract and reach a voicemail that’s no longer monitored. Or the company has rebranded. Or they’re deployed in Ohio chasing the next storm.

You have a warranty on paper. You have no one to honor it. Before signing any contract, Google the company name plus their city of origin, check BBB for address history, and call the number during business hours to ask where the local project manager is physically based.

5. They Create Insurance Complications That Follow You

Inflated or fraudulent insurance claims filed by storm chasers can affect a homeowner’s claims history and future premiums. Some Cypress homeowners whose storm chaser contractors filed inflated supplemental claims have received policy non-renewal notices from their insurer. This is a consequence most homeowners don’t anticipate. The damage to their insurance relationship outlasts the contractor by years. In Harris County, which has among the highest claim densities in Texas, insurers pay close attention to claim patterns.

Want to understand how legitimate insurance claims work and what to watch for? Read whether to contact insurance or a roofer first. The decision affects both your claim outcome and your exposure to this kind of risk.

What M&M Finds When Called to Fix Storm Chaser Work in Cypress

M&M now conducts a storm chaser audit as part of any inspection on a Cypress roof replaced within the past three years. In roughly one in four recent replacements inspected in Cypress, at least one material discrepancy from what insurance paid for turns up.

The Shingle Swap. A Bridgeland home, 14 months after a “new roof” following a 2024 hail event. The homeowner calls M&M, reporting granule loss faster than expected. The roof gets walked. The shingles are 3-tab, identifiable by the flat, single-layer profile and uniform tab pattern. The insurance estimate from 14 months prior specified GAF Timberline HDZ dimensional shingles. The storm chaser installed 3-tab, pocketed the difference, and left. The 3-tab shingles are already showing stress cracks from Cypress’s thermal cycling. Estimated remaining life: five to seven years. The architectural shingles they were paid for would have provided 25 to 30.

The Missing Drip Edge. A Towne Lake home, 18 months after a “full roof replacement.” Fascia rot is developing along the eave line. M&M pulls back the first row of shingles at the eave. No drip edge. It was specified in the insurance estimate and paid for. Without a drip edge, water wicks back under the first shingle course into the fascia with every rain event. Fascia replacement on a home that size adds $1,200 to $2,500 to the true repair cost. The storm chaser is unreachable.

These aren’t isolated cases. They’re patterns documented on Cypress roofs across multiple storm seasons, by contractors who knew the homeowner couldn’t identify the difference from the ground and wouldn’t check until something went wrong.

Already had roof work done and want to know what was actually installed? Request a free post-replacement audit from M&M →

How to Verify a Roofing Contractor in Cypress Before You Sign Anything

These six steps take less than 30 minutes. They’re the difference between the homeowners in these examples and the ones who didn’t have problems.

Step 1: Verify their Texas contractor license through TDLR. Go to license.tdlr.texas.gov. If they’re not licensed in Texas, stop the conversation. This takes two minutes.

Step 2: Confirm a physical Texas address. Not a P.O. box. Not “serving the Houston area” with an address that Street View reveals as a residential house in another state. Ask for the address and look it up.

Step 3: Check how long they’ve been operating in Texas. A contractor who opened a Texas LLC six weeks ago is not a local contractor. BBB shows the founding date. The Texas Secretary of State business search shows the registration date. Both are public records.

Step 4: Never sign an Assignment of Benefits before a complete scope of work is in writing. If a contractor requires an AOB before providing a written scope, walk away.

Step 5: Ask for three local Cypress or Harris County references from jobs completed in the past 12 months. A legitimate local contractor has them readily available. A storm chaser does not.

Step 6: Know your deductible rights. Under Texas House Bill 2102, it’s illegal for any roofing contractor to offer to cover your deductible. [3] Any contractor making this offer is in violation of state law, and it’s a reliable indicator of broader fraudulent practices.

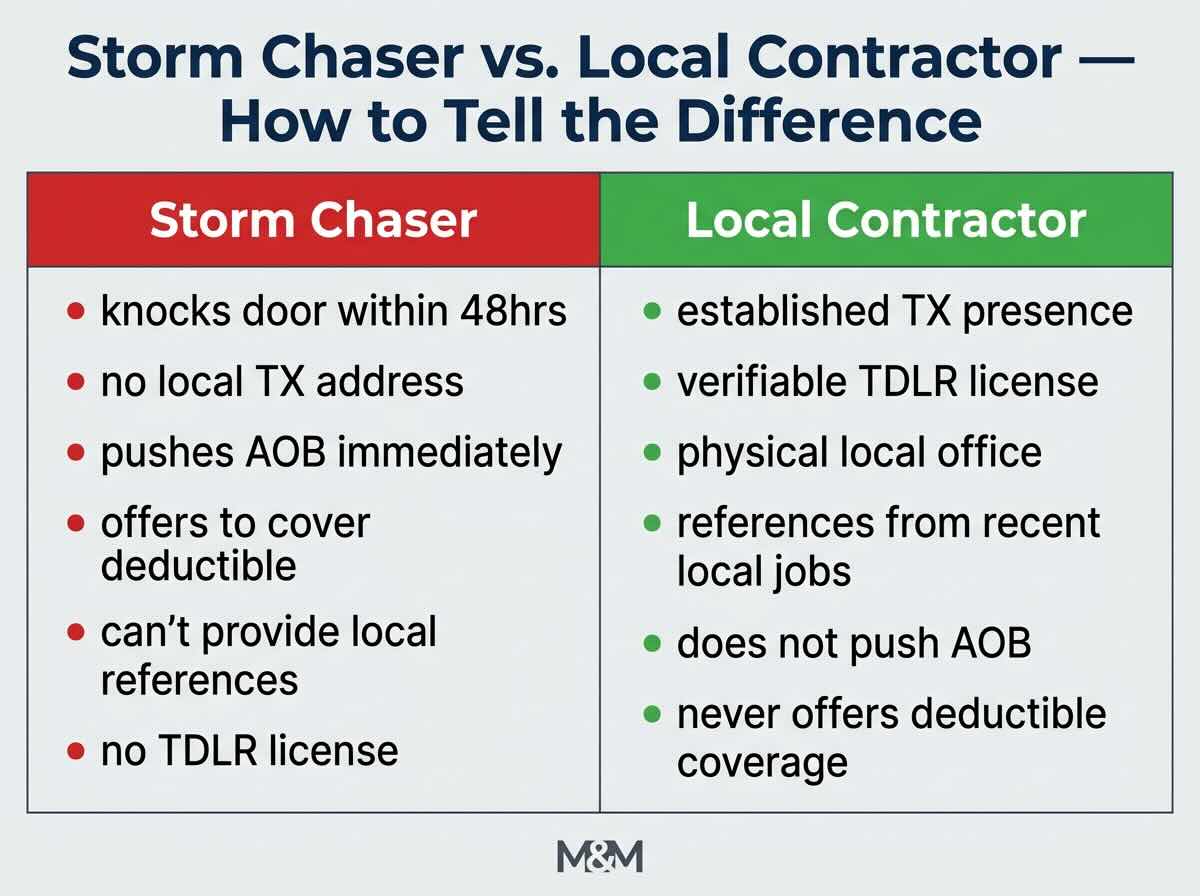

| Storm Chaser | Legitimate Local Contractor |

|---|---|

| Arrives door-to-door within 48 hrs of storm | Has permanent presence in your market |

| No verifiable physical TX address | Local office, verifiable on Street View |

| Pushes AOB before any inspection | Does not require AOB for standard work |

| Offers to cover your deductible (illegal in TX) | Never makes this offer |

| Can’t provide recent local Cypress references | Local references available on request |

| Unreachable 6–12 months after completion | Permanent local presence + lifetime warranty |

| No TDLR license or recent TX registration | TDLR-verifiable license, years of TX operation |

M&M Roofing has served the Greater Houston market, including Cypress and northwest Harris County, since 1983. Not since the last storm. Since 1983. That’s 40+ years in this market, 100,000+ completed projects, and a roofing contractor presence in Houston built entirely on being here when something goes wrong six months from now.

Doug Moncure, M&M’s owner, personally calls every client after project completion. When a shingle blows off next spring, that’s not a warranty card in a drawer. It’s a company that answers the phone, has the project file, and sends someone out. M&M backs all new roof installations with a lifetime labor warranty. Schedule your free inspection →

The Bottom Line for Cypress Homeowners

Cypress’s storm activity has made it a target. The homeowners who get burned aren’t naive. They just weren’t given the tools to tell the difference between a legitimate local company and a sophisticated operation that’s run this play hundreds of times.

The checklist in this article changes that. Verify the license. Confirm the physical address. Check the Texas registration date. Don’t sign an AOB before you have a written scope. Ask for local references.

And if your roof was replaced in the last three years and you’re not sure what was actually installed, M&M can tell you. The audit inspection is free. See why Cypress homeowners trust M&M — schedule your inspection today →

Frequently Asked Questions

How do I know if the roofing company knocking on my door in Cypress is legitimate?

Verify their Texas contractor license at license.tdlr.texas.gov. Confirm a physical Texas office address, not a P.O. box. Ask how long they’ve been operating in Harris County. Legitimate local contractors have years of verifiable history and recent Cypress references on request.

Is it illegal for a roofer to offer to cover my deductible in Texas?

Yes. Under Texas House Bill 2102, effective September 1, 2019, it’s a criminal offense for a roofing contractor to offer, waive, or absorb a homeowner’s insurance deductible as an inducement to use their services. Any contractor making this offer is violating Texas law. Report them to the Texas Attorney General’s Consumer Protection Hotline at 800-621-0508.

What is an Assignment of Benefits, and should I sign one?

An AOB transfers your right to insurance proceeds from you to the contractor, allowing them to negotiate and collect your insurance payment directly. Never sign an AOB before you have a complete, written scope of work specifying exact materials and costs. Legitimate local contractors do not require AOB agreements to proceed with standard roof work.

How do I check if my new roof has the right materials after a storm chaser replacement?

Ask M&M Roofing for a post-replacement audit inspection. We check the installed shingle product against what was specified in the insurance estimate, verify drip edge installation, confirm ice and water shield placement, and assess flashing. If your roof was replaced within the last three years and you’re uncertain what was installed, a free inspection answers that question.

How long has M&M been serving the Cypress area?

M&M Roofing has served the Greater Houston market, including Cypress and northwest Harris County, since 1983. This is our permanent market.

References

[1] Bailey Roofing & Construction — Guide to Handling the Christmas Eve Hailstorm in Cypress, TX

[2] Texas Department of Insurance — Roofing and Insurance: Know the Law

[3] Texas Department of Insurance — New State Law Cracks Down on Roof Scams

M&M Roofing, Siding & Windows has served homeowners across Texas and Louisiana for more than 40 years. Backed by over 100,000 completed home improvement projects, M&M offers expert insight on roofing, siding, windows, gutters, storm damage, and exterior restoration, helping homeowners make confident, informed decisions about their property.